International Long-Term Care Benefits: Hybrid LTC Policies .

More and more people are considering retiring abroad, drawn by the allure of a lower cost of living, diverse cultures, and picturesque surroundings. However, one crucial aspect of retiring overseas that is often overlooked is the need for long-term care (LTC) insurance. In this blog post, we will discuss the importance of having a long-term care insurance policy when living overseas and the factors to consider when selecting a policy to ensure you’re adequately covered.

The Importance of Long-Term Care Insurance Abroad

As people age, the likelihood of needing assistance with daily activities or medical care increases. Long-term care insurance policies are designed to cover these costs, helping to protect your finances and ensure that you receive the care you need. When living overseas, having an LTC policy that covers international care is even more critical due to factors such as:

- Differences in healthcare systems: Healthcare systems vary significantly between countries, and the quality and cost of care can differ substantially. An LTC policy with international coverage can help mitigate these uncertainties and ensure that you receive the care you need.

- Limited access to government assistance: Many countries do not provide the same level of government assistance for long-term care as the United States, making it essential to have a private insurance policy in place.

- Expatriate status: Some countries may have specific residency requirements or restrictions for expatriates accessing local healthcare services, making it crucial to have an LTC policy that covers care in your chosen country.

Factors to Consider When Choosing an LTC Policy for Overseas Living

- International coverage: When selecting an LTC policy, ensure it includes international coverage or has provisions for care in your chosen country. Not all policies provide coverage outside the United States, so it’s essential to verify this feature.

- Currency exchange rates: Be aware that fluctuations in exchange rates can impact the value of your LTC policy benefits. Consider choosing a policy that provides benefits in the local currency or includes provisions to adjust for currency fluctuations.

- Inflation protection: With the cost of care rising worldwide, it’s essential to select a policy that offers inflation protection. This feature helps your benefits keep pace with the increasing costs of care, ensuring that you’re adequately covered as you age.

- Provider network: Investigate the provider network of your chosen insurance policy to ensure it includes reputable care providers in your chosen country. This ensures that you receive high-quality care when needed.

- Benefit triggers: Review the benefit triggers of your policy, which determine when you become eligible for benefits. Ensure they align with the healthcare system in your chosen country and can be easily met while living abroad.

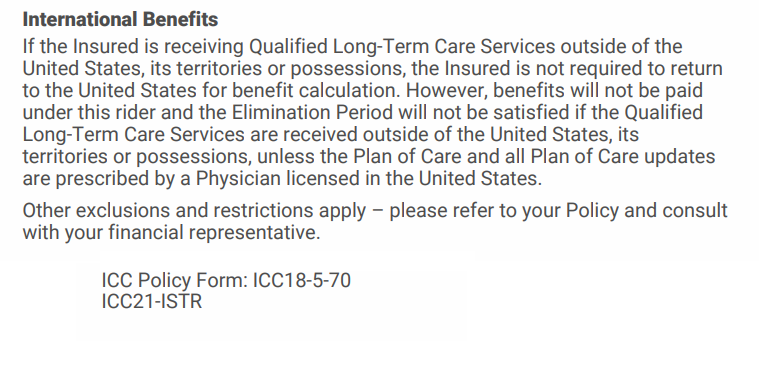

The Best Overall Company for International Benefits

Based on our 2023 analysis of the landscape of Hybrid LTC providers, we award the best and most clear International Benefits provision to Brighthouse. Here is what they say in their illustration:

To request a Brighthouse quote, click here.

Conclusion

Securing a long-term care insurance policy with international coverage is an essential aspect of planning for retirement overseas. By considering factors such as international coverage, currency exchange rates, inflation protection, provider networks, and benefit triggers, you can ensure that you’re adequately protected, regardless of where you choose to retire. With proper planning and the right LTC policy, you can enjoy a worry-free retirement in your dream destination.

Table of Contents